280e tax compliance

Compliance with Section 280E of the Internal Revenue Code presents a significant challenge for businesses operating in industries deemed illegal under federal law, particularly cannabis enterprises. Enforced since 1982, 280E prohibits taxpayers from deducting ordinary business expenses if their income stems from a federally prohibited substance.

This restriction severely impacts profitability, as companies must pay federal income tax on gross revenue minus only the cost of goods sold. Despite state-level legalization in many areas, 280E remains a barrier to financial stability and growth. Navigating this complex regulation requires meticulous record-keeping, strategic planning, and a thorough understanding of IRS guidelines to remain in compliance while minimizing tax liability.

Understanding 280E Tax Compliance in the Cannabis Industry

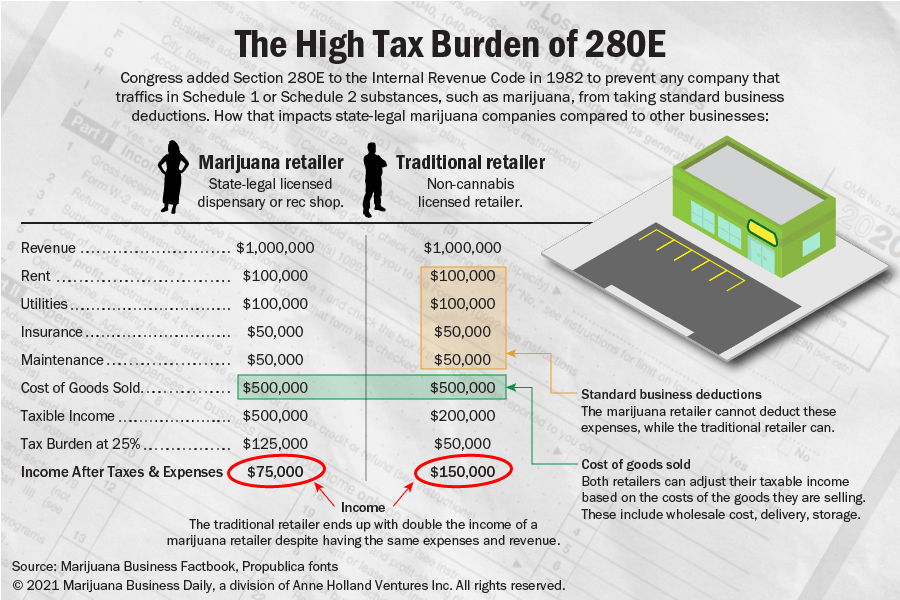

The Internal Revenue Code Section 280E presents a significant challenge for businesses operating in the U.S. cannabis sector, prohibiting these entities from deducting most standard business expenses on their federal tax returns.

Enforced since 1982, this tax code provision was originally designed to prevent drug dealers from claiming tax write-offs, but it now applies broadly to state-legal marijuana businesses due to cannabis's continued classification as a Schedule I controlled substance under federal law. As a result, cannabis retailers, producers, and distributors must pay federal income taxes on their gross profits rather than net income, dramatically increasing their effective tax rates—sometimes exceeding 70%.

Despite generating legitimate revenue through compliant operations, these businesses face intense financial pressure due to their inability to claim deductions for rent, payroll, advertising, and other ordinary operational costs, making 280E tax compliance a central concern for sustainable growth in the industry.

What Is Section 280E of the Internal Revenue Code?

Section 280E of the Internal Revenue Code explicitly disallows businesses from claiming tax deductions or credits for expenses related to trafficking in controlled substances listed under Schedule I or II of the Controlled Substances Act.

While the law was enacted to target illegal drug operations, the federal classification of marijuana as a Schedule I substance means that even state-legal cannabis businesses are subject to its restrictions.

The IRS interprets this broadly, preventing deductions for nearly all standard operating expenses—except for the cost of goods sold (COGS)—even when businesses follow state regulations and generate legal revenue. This creates a significant disparity between cannabis operations and other legal industries, where deductions are standard. The lack of clarity and evolving legal status of cannabis continue to fuel debates over fairness and economic viability under this provision.

Permitted Deductions Under 280E: The Role of Cost of Goods Sold

Although Section 280E blocks the deduction of most operating expenses, the IRS allows cannabis businesses to calculate and deduct the cost of goods sold (COGS), providing a limited but crucial avenue for tax reduction.

COGS includes direct costs inherent to producing or acquiring products for sale, such as raw materials, packaging, cultivation labor, and manufacturing overhead. Properly structuring COGS under IRS guidelines—particularly following Treasury Regulation §1.471-11—can significantly lower taxable income, as these costs are subtracted before gross profit is calculated.

For example, businesses may include expenses such as soil, nutrients, containers, and direct labor in growing operations as part of COGS. Maximizing allowable COGS is therefore a cornerstone of 280E tax compliance, requiring detailed record-keeping, inventory tracking, and a solid understanding of tax regulations to withstand IRS scrutiny.

Cannabis businesses must adopt strategic financial and operational frameworks to remain compliant with Section 280E while minimizing tax liability.

Key approaches include accurately allocating expenses between non-deductible operating costs and allowable COGS, utilizing separate entities for ancillary services (e.g., management or consulting), and ensuring complete financial transparency through specialized accounting systems. Some companies structure their operations to segregate cannabis and non-cannabis revenue streams, allowing for standard deductions in federally legal business segments.

Additionally, meticulous documentation and tax planning with professionals experienced in cannabis taxation are essential to defend against audits and maximize legal leeway. Emerging legislative efforts such as the Cannabis Business Supply Chain, Expungement, and Regulation (CASPER) Act may offer future relief, but until federal reform occurs, proactive compliance and financial innovation remain critical.

| Tax Consideration | Applicability to Cannabis Businesses | Key Notes |

|---|---|---|

| Section 280E Restriction | Applies to all cannabis-related businesses | Bars deductions for rent, marketing, payroll, insurance, and most overhead |

| Cost of Goods Sold (COGS) | Permitted deduction | Includes cultivation materials, direct labor, packaging; must follow IRS inventory rules |

| State-Legal Operations | Still subject to federal tax rules | No protection from 280E despite compliance with local laws |

| IRC Section 263A (UNICAP) | Applies to inventory valuation | Requires capitalization of certain indirect costs into COGS for tax calculation |

| Tax Rates | Often exceeds 70% | Due to taxation on gross profit, not net income |

Comprehensive Guide to 280E Tax Compliance for Businesses

What are the tax liabilities under Section 280E for compliant cannabis businesses?

Understanding Section 280E and Its Application to Cannabis Businesses

- Section 280E of the U.S. Internal Revenue Code disallows businesses from claiming most ordinary and necessary business deductions if they are trafficking in controlled substances as defined by the Controlled Substances Act (CSA), which includes cannabis, despite its legality under certain state laws.

- Because marijuana remains classified as a Schedule I substance at the federal level, even state-compliant cannabis businesses are subject to Section 280E, meaning they cannot deduct typical business expenses such as rent, advertising, payroll, or utilities from their gross income when filing federal taxes.

- As a result, these businesses often face significantly higher effective tax rates—sometimes exceeding 70%—because taxable income is calculated on gross profit (revenue minus cost of goods sold) without the benefit of reducing income through standard operating expense deductions.

Limited Deductions Allowed Under Section 280E: The Role of Cost of Goods Sold (COGS)

- While Section 280E prohibits most business expense deductions, it does not restrict the deduction of the cost of goods sold (COGS), which allows cannabis businesses to reduce gross income by expenses directly tied to the production of their inventory.

- Permitted COGS components may include costs such as raw materials, direct labor involved in cultivation or manufacturing, packaging, transportation of goods, and certain overhead expenses allocable to production, provided they meet IRS criteria under Section 471 and related regulations.

- This narrow allowance creates a strong incentive for cannabis businesses to maximize qualifying COGS allocations, often leading to complex accounting practices and careful documentation to withstand potential IRS scrutiny during audits.

Tax Compliance Strategies for Cannabis Businesses Under Section 280E

- Many compliant cannabis businesses employ specialized tax accounting methods to categorize as many expenses as possible within COGS, thus gaining partial relief from the harsh limitations of Section 280E while remaining within legal boundaries.

- Federal tax filings still require cannabis businesses to report all income, often resulting in high tax bills despite limited deductions. As a result, businesses must maintain precise financial records and may need to use methods like the Uniform Capitalization (UNICAP) rules to properly allocate costs.

- Some businesses also explore entity structuring or ancillary operations—such as consulting or real estate leasing—through separate legal entities to allow for full deductions in non-cannabis-related income streams, although this must be done carefully to avoid IRS challenges related to substance-over-form doctrines.

Is Section 280E still applicable for tax compliance in 2024?

Yes, Section 280E of the Internal Revenue Code remains applicable for federal tax compliance in 2024. Despite ongoing legislative discussions and attempts to reform cannabis-related tax policies, Section 280E has not been repealed or substantially amended at the federal level.

This provision prohibits businesses that are trafficking in controlled substances—classified under Schedule I or II of the Controlled Substances Act—from claiming most ordinary business deductions and credits on their federal income tax returns.

Since cannabis remains classified as a Schedule I substance under federal law, cannabis businesses, even those operating legally under state laws, are still subject to the restrictions imposed by Section 280E. As a result, companies in the cannabis industry continue to face significantly higher effective tax rates compared to other industries due to the disallowance of deductions for expenses such as rent, payroll (except wages), marketing, and general business operations.

What Is Section 280E and How Does It Impact Cannabis Businesses?

- Section 280E was introduced in 1982 as part of the Tax Equity and Fiscal Responsibility Act, originally aimed at preventing drug traffickers from deducting business expenses. Its application to state-legal cannabis businesses arose after the IRS determined that because marijuana remains federally illegal, businesses selling it cannot benefit from standard tax deductions.

- The practical effect of Section 280E means that while cannabis companies can deduct the cost of goods sold (COGS) under IRS Chief Counsel Memorandum 200739001, they are barred from deducting most other legitimate business expenses such as advertising, travel, professional services, insurance, and utilities.

- This limitation results in effective tax rates that can exceed 70% in some cases, even in profitable operations, creating a major financial burden and disincentivizing transparency and reporting in an industry striving for legitimacy.

Are There Any Exceptions or Workarounds Under Section 280E in 2024?

- One key exception permitted under Section 280E is the deduction of cost of goods sold (COGS), which allows businesses to allocate certain direct production, purchase, and resale costs, provided they follow proper inventory accounting methods and comply with Section 471 of the tax code.

- Some multi-state operators have strategically structured their businesses by separating state-legal cannabis activities from ancillary services (like consulting, management, or real estate) to allow the ancillary arms to claim full deductions since they do not directly handle cannabis.

- Additionally, the SCOBE Act (Still Cannabis Operators Business Expenses) and other proposals have been introduced in Congress to extend deductions to state-compliant cannabis businesses, but as of 2024, none have passed into law, leaving current workarounds as the primary relief available.

What Legislative Changes Are Being Considered to Modify Section 280E?

- The most notable legislative effort is the passage of the Cannabis Administration and Opportunity Act (CAOA), which, among broader reforms, includes provisions to repeal or modify Section 280E for businesses operating in compliance with state cannabis laws. However, this bill has not advanced to enactment as of 2024.

- Separately, the bipartisan Secure and Fair Enforcement (SAFE) Banking Act, while primarily focused on financial services access, has often been bundled with tax reform discussions, including amendments to Section 280E, though standalone passage has not yet occurred.

- The IRS and Treasury Department continue to monitor the situation, but no administrative relief has been issued. State-level tax regimes are increasingly diverging, with many states allowing full deductions to support local cannabis economies, highlighting the ongoing disconnect between federal policy and state implementation.

Which states have tax codes decoupled from federal 280E for cannabis businesses?

States with Full or Partial Decoupling from Federal 280E

- Several states have taken legislative action to decouple from the federal tax code regarding Internal Revenue Code Section 280E, which denies tax deductions to businesses trafficking in federally illegal controlled substances, including cannabis. As of the most recent updates, states like California, Colorado, Maine, Nevada, and Washington have implemented either full or partial decoupling measures to provide relief to state-licensed cannabis businesses.

- In California, the state allows cannabis businesses to deduct ordinary business expenses despite federal restrictions, effectively creating a separate state-level tax calculation that does not follow 280E. Similarly, Colorado passed legislation that permits cannabis operators to use federal deductions when calculating state income tax, easing the financial burden at the state level.

- Other states with partial decoupling include Illinois, Maryland, and New Jersey. These states typically allow deductions for expenses such as rent, payroll, and overhead when calculating state income tax, even though they remain technically subject to 280E under federal law. This distinction allows cannabis businesses to operate with improved cash flow and better financial planning at the state level.

How Decoupling Impacts Cannabis Business Taxation

- Decoupling from federal 280E allows state-licensed cannabis companies to claim deductions for standard business expenses—such as employee wages, utilities, marketing, and rent—on their state tax returns. Without this relief, these businesses would be forced to pay state income taxes on gross revenue rather than net income, leading to disproportionately high tax burdens.

- The ability to deduct operational expenses reduces effective tax rates and improves profitability, making the legal cannabis market more competitive with the illicit market. States that decouple often see increased compliance, as businesses are more willing to operate transparently within the legal framework when tax policies are economically sustainable.

- Furthermore, decoupling enhances transparency and recordkeeping because businesses are incentivized to maintain detailed financial records to substantiate deductions. This improves oversight for state regulators and supports the long-term viability of the legal cannabis industry by fostering a more business-friendly environment.

Legislative Trends and Emerging States Considering Decoupling

- Recent legislative sessions in states like Michigan, Massachusetts, and New York have included proposals aimed at decoupling from 280E, reflecting a growing recognition of the inequities faced by cannabis businesses. While some have fully adopted decoupling, others are exploring hybrid models that limit certain deductions while allowing essential operating costs to be written off.

- States with adult-use legalization that have not yet fully decoupled are under increasing pressure from industry stakeholders to adjust their tax codes. Advocacy groups argue that without decoupling, small and social equity-owned businesses face insurmountable financial challenges that hinder diversity and equitable growth in the legal market.

- Moving forward, the trend suggests more states will reconsider their alignment with federal 280E as the legal cannabis industry matures. Legislative action is especially likely in newly legal markets like Virginia and Connecticut, where lawmakers are crafting tax frameworks with lessons learned from earlier-legalized states.

What is the Safe Banking Act and How Does It Relate to 280E Tax Compliance?

What Is the Safe Banking Act and Its Purpose?

- The Safe Banking Act, formally known as the Secure and Fair Enforcement (SAFE) Banking Act, is proposed legislation in the United States designed to allow cannabis-related businesses in states where marijuana is legal to access traditional banking services without fear of federal prosecution or penalties.

- Currently, due to cannabis remaining classified as a Schedule I controlled substance under federal law, many financial institutions are hesitant to serve cannabis companies, fearing violations of anti-money laundering laws and federal regulations. This has forced many cannabis operators to operate primarily in cash, increasing risks related to theft, security, and financial transparency.

- The SAFE Banking Act aims to protect banks, credit unions, and other financial institutions that choose to work with state-compliant cannabis businesses by prohibiting federal regulators from penalizing them solely for providing services to these entities, thereby enhancing safety, accountability, and regulatory oversight in the industry.

How Does Section 280E of the Internal Revenue Code Impact Cannabis Businesses?

- Section 280E of the U.S. Internal Revenue Code disallows businesses from deducting ordinary business expenses—such as rent, advertising, payroll, and utilities—if they are involved in the sale of substances classified as Schedule I or II drugs under federal law, which includes cannabis.

- This restriction results in cannabis businesses being taxed on their gross income rather than net income, significantly increasing their effective tax rates and reducing their profitability compared to businesses in other industries.

- Even businesses operating legally under state law are subject to 280E, creating a major financial burden and complicating financial planning. Some limited workarounds exist, such as cost of goods sold deductions allowed under IRS rulings, but these do not offset the full impact of 280E.

Connection Between the Safe Banking Act and 280E Tax Challenges

- While the Safe Banking Act does not directly repeal or modify Section 280E, it is part of a broader conversation about normalizing the financial operations of state-legal cannabis businesses—normalization that could pave the way for eventual reform of burdensome tax policies like 280E.

- Improved banking access allows for better financial record-keeping, transparency, and audit trails, which could assist cannabis operators in navigating complex tax compliance under 280E by providing clearer documentation of allowable deductions and revenue streams.

- Advocates argue that passage of the Safe Banking Act would signal growing federal acceptance of the legal cannabis industry, increasing political momentum for comprehensive tax reform, including adjustments or repeal of Section 280E, to reflect the evolving state-federal landscape of cannabis legalization.

Frequently Asked Questions

What is 280E tax compliance?

280E tax compliance refers to adhering to Section 280E of the U.S. Internal Revenue Code, which prohibits businesses selling federally illegal drugs from deducting most business expenses. This impacts cannabis companies, as they can only deduct cost of goods sold.

Compliance requires accurate reporting to avoid audits and penalties, even though state legality may differ. Proper accounting is essential to meet IRS standards while operating legally at the state level but restricted federally.

Why can't cannabis businesses claim standard deductions under 280E?

Cannabis businesses cannot claim standard tax deductions under 280E because marijuana remains a Schedule I controlled substance federally. The IRS enforces this code section by disallowing deductions for operating expenses like rent, advertising, or salaries.

Only the cost of goods sold (COGS) is deductible. This results in significantly higher effective tax rates. Companies must maintain precise financial records to justify allowable deductions and ensure compliance with federal tax laws despite state legalization.

How does 280E affect cannabis company profitability?

280E greatly reduces cannabis company profitability by disallowing deductions for common business expenses such as payroll, marketing, and rent. As a result, taxable income is much higher, leading to effective tax rates that can exceed 70%.

This financial burden limits growth, reinvestment, and competitiveness, especially compared to businesses in legal industries. Strategic accounting and structuring, such as separating state-legal operations from federal reporting, are often needed to mitigate its impact.

Are there any strategies to minimize 280E tax burdens?

Yes, businesses can minimize 280E tax burdens by maximizing allowable cost of goods sold (COGS) deductions and separating deductible vs. non-deductible expenses. Some use vertical integration to allocate more costs to COGS.

Others structure operations so that ancillary services are taxed separately. Working with experienced cannabis accountants and using IRS-compliant accounting methods like the IRC Section 471 inventory method can help. However, all strategies must remain within IRS guidelines to avoid audits or penalties.

Leave a Reply