Accounting and tax compliance

Navigating the complex landscape of accounting and tax compliance is essential for businesses of all sizes. Accurate financial reporting and adherence to tax regulations not only ensure legal conformity but also build trust with stakeholders and authorities.

With evolving tax laws and stringent reporting requirements, maintaining compliance demands vigilant oversight and up-to-date knowledge. Failure to comply can result in penalties, audits, or reputational damage.

Effective accounting practices serve as the foundation for timely tax filings, strategic financial planning, and regulatory transparency. This article explores key aspects of accounting and tax compliance, offering insights into best practices that help organizations remain compliant, efficient, and prepared in today’s dynamic fiscal environment.

Ensuring Accuracy and Legality: The Importance of Accounting and Tax Compliance

Maintaining proper accounting and tax compliance is a cornerstone of responsible business operations. Accurate financial records not only reflect a company’s true economic status but also ensure adherence to legal and regulatory standards set by governing bodies such as the IRS in the United States or HMRC in the UK.

Failure to comply can result in severe penalties, audits, reputational damage, and even criminal charges. Effective accounting systems capture all financial transactions—including revenue, expenses, assets, and liabilities—while tax compliance ensures that the correct amount of tax is calculated, reported, and paid on time.

Businesses must stay updated with evolving tax codes, reporting requirements, and deadlines to avoid non-compliance. Moreover, compliance fosters transparency with stakeholders such as investors, creditors, and regulators, building trust and credibility in the marketplace.

Core Components of Financial Accounting for Compliance

The foundation of tax compliance lies in robust financial accounting practices that track and organize monetary transactions systematically.

Key components include maintaining a general ledger, preparing trial balances, generating financial statements such as the balance sheet, income statement, and cash flow statement, and adhering to standardized accounting principles like GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards). These documents not only provide internal insights into business performance but are also essential for external reporting and tax filings.

Accurate accounting ensures that all income is recorded, expenses are properly categorized, and assets and liabilities are correctly valued—critical elements when calculating taxable income. Automation through accounting software enhances precision, reduces errors, and streamlines audit readiness.

Meeting Tax Filing Requirements and Deadlines

Timely and accurate tax filing is a fundamental aspect of tax compliance, requiring businesses to submit various forms and reports based on their structure and jurisdiction.

Whether a business is a sole proprietorship, partnership, corporation, or LLC, it must comply with federal, state, and local tax obligations including income tax, sales tax, payroll tax, and estimated tax payments. For instance, in the U.S., corporations must file Form 1120, while sole proprietors report business income on Schedule C attached to Form 1040.

Employers must also file quarterly Form 941 for payroll taxes and annually Form 940 for FUTA taxes. Missing deadlines can lead to penalties and interest charges. Therefore, using tax calendars and automated reminders is crucial to maintaining compliance and avoiding unnecessary financial burdens.

Managing Audits and Regulatory Scrutiny

Even with diligent compliance efforts, businesses may face audits from tax authorities to verify the accuracy of reported financial information. A tax audit can be triggered by random selection, anomalies in tax returns, or industry-specific scrutiny.

Being prepared involves maintaining organized financial records, preserving documentation such as invoices, receipts, bank statements, and prior tax returns for the required retention period—typically three to seven years. During an audit, transparency and cooperation are vital; having a qualified tax professional or CPA assist can greatly improve outcomes.

Proactive measures like internal audits and compliance reviews can identify and correct issues before they escalate. Demonstrating consistent adherence to accounting standards and tax regulations reduces the risk of adverse findings and reinforces organizational integrity.

| Compliance Area | Key Requirement | Common Deadline (U.S.) | Potential Penalty |

|---|---|---|---|

| Income Tax Filing | Annual reporting of business profits and losses | April 15 (Form 1040, 1120, 1065) | 5% per month of unpaid tax (up to 25%) |

| Payroll Tax | Withholding and remitting employee taxes | Quarterly (Form 941), Annually (Form 940) | 2% to 15% of unremitted amount |

| Sales Tax | Collecting and submitting sales tax to state | Monthly/Quarterly (varies by state) | Interest plus penalty up to 25% |

| Record Retention | Preservation of financial documentation | 3–7 years after filing | Fines or disallowed deductions |

Understanding Accounting and Tax Compliance: A Comprehensive Guide

What does tax compliance mean in accounting?

Tax compliance in accounting refers to the process by which individuals, businesses, and organizations adhere to the tax laws and regulations established by governmental authorities. This includes accurately calculating taxes owed, filing tax returns on time, maintaining proper documentation, and making timely payments.

Compliance ensures that taxpayers meet their legal obligations and avoid penalties, audits, or legal consequences. In accounting, tax compliance is integrated into financial reporting and internal controls to ensure alignment between financial statements and tax filings. It involves ongoing monitoring of tax legislation changes and implementing procedures that support consistent, transparent, and lawful tax practices.

Key Components of Tax Compliance

- Accurate income reporting: Taxpayers must report all sources of income correctly, including wages, business revenue, investment gains, and other taxable earnings. This ensures the tax base is complete and aligns with legal requirements.

- Proper deduction and credit application: Claiming eligible deductions and tax credits is part of compliance, but these must be substantiated with valid records and meet specific criteria set by tax authorities.

- Timely filing and payment: Meeting all deadlines for submitting tax returns and paying taxes due is fundamental. Late filings or payments can result in interest charges, fines, or further scrutiny from tax agencies.

Role of Accountants in Tax Compliance

- Advising on tax strategy: Accountants help clients structure their financial affairs in a legal and tax-efficient way, ensuring strategies remain within the boundaries of the law while minimizing tax liabilities.

- Maintaining accurate records: Accountants are responsible for organizing and preserving financial documentation that supports tax positions, such as receipts, ledgers, and income statements.

- Preparing and reviewing tax returns: Professionals ensure that all forms are completed accurately and filed on schedule, reducing the risk of errors that could trigger audits or penalties.

Consequences of Non-Compliance

- Financial penalties: Tax authorities impose fines and interest on unpaid or late taxes, which can significantly increase the total amount owed over time.

- Audits and investigations: Inconsistent reporting or suspicious filings may lead to audits, requiring extensive documentation and potentially uncovering additional issues.

- Legal and reputational risks: Severe non-compliance, such as tax evasion, can result in criminal charges, legal action, and damage to a business’s or individual’s reputation, affecting future financial opportunities.

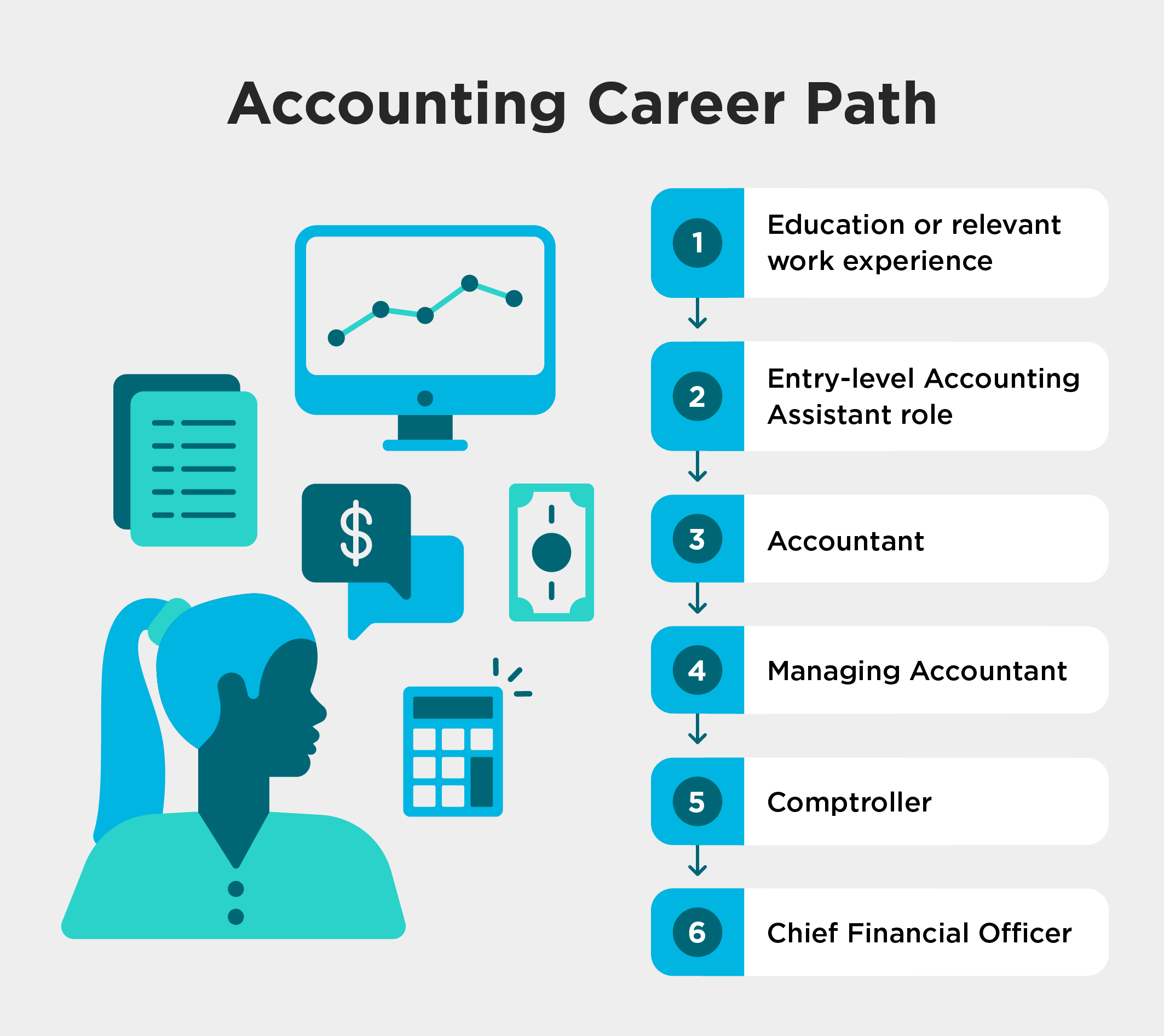

Is a career in accounting and tax compliance a strong professional choice?

Yes, a career in accounting and tax compliance is widely considered a strong professional choice due to its stability, demand, and opportunities for advancement.

This field forms the backbone of financial integrity in organizations across all sectors, ensuring that businesses and individuals meet legal obligations while optimizing financial performance. With evolving tax regulations, increasing financial transparency requirements, and global economic complexity, professionals in this domain play a critical role.

The career offers multiple pathways, including public accounting, corporate finance, government roles, and consulting, allowing individuals to specialize based on interest and expertise. Additionally, certifications like CPA (Certified Public Accountant) or EA (Enrolled Agent) enhance credibility and open doors to higher earning potential and leadership positions.

Job Stability and Demand in Accounting and Tax Compliance

- Accounting and tax compliance professionals are consistently in demand because all organizations—regardless of size or industry—must adhere to tax laws and maintain accurate financial records, creating a steady need for skilled practitioners.

- Economic fluctuations tend to have less impact on this field compared to others, as tax obligations persist in both growth and recession periods, leading to greater job security.

- Seasonal demand, particularly during tax filing periods, further underscores the necessity of these roles, with many firms expanding their workforce temporarily or permanently to manage increased workloads.

Opportunities for Career Advancement and Specialization

- Professionals can progress from entry-level positions such as junior accountant or tax associate to senior roles like audit manager, tax director, or chief financial officer (CFO), depending on experience and qualifications.

- Specializations in areas such as international tax, forensic accounting, mergers and acquisitions, or environmental compliance allow individuals to develop niche expertise that is highly valued in the market.

- Ongoing education and certifications not only improve job prospects but also position individuals for consulting roles or launching independent practices, offering flexibility and entrepreneurial opportunities.

Impact of Technology and Regulatory Changes

- Advancements in accounting software, artificial intelligence, and data analytics are transforming the field, enabling professionals to focus more on strategic advisory roles rather than routine data entry.

- Accounting and tax compliance experts must stay current with evolving regulations, such as changes in tax codes, anti-money laundering laws, and international reporting standards like IFRS and GAAP.

- The increasing globalization of business means professionals often deal with cross-border taxation and compliance, making knowledge of international regulations a valuable asset in expanding career options.

What Are the Key Components of Tax Compliance in Accounting?

Accurate Record-Keeping and Documentation

Maintaining accurate financial records is a foundational element of tax compliance in accounting. Without reliable documentation, businesses face the risk of errors, audits, and penalties. Proper record-keeping ensures that all financial transactions are captured, categorized correctly, and available for review during tax preparation or inspections by tax authorities.

- Every business must systematically track income, expenses, assets, and liabilities using accounting software or manual ledgers to ensure data integrity and traceability.

- Supporting documents such as invoices, bank statements, receipts, and payroll records should be retained for a legally mandated period—typically five to seven years depending on jurisdiction.

- Organized documentation facilitates easier preparation of tax returns and provides crucial evidence in case of disputes or audits with tax agencies.

Timely Filing and Payment of Taxes

Meeting filing deadlines and ensuring timely payment of taxes are essential components of tax compliance. Late filings or unpaid taxes can result in penalties, interest charges, or legal consequences, damaging both the financial health and reputation of a business.

- Businesses must adhere to specific due dates for federal, state, and local tax returns, such as income tax, sales tax, and payroll tax filings, which vary based on entity type and location.

- Estimating tax liabilities accurately and making quarterly estimated payments—when required—helps avoid underpayment penalties and cash flow issues at year-end.

- Utilizing electronic filing (e-file) and electronic payment systems improves accuracy, efficiency, and provides proof of submission on time.

Adherence to Tax Laws and Regulatory Updates

Tax regulations are subject to frequent changes at both national and international levels, making it imperative for accountants and businesses to remain updated on legislative developments. Non-compliance due to ignorance of current laws can lead to significant financial and legal repercussions.

- Accounting professionals must regularly monitor updates from tax authorities such as the IRS in the U.S. or HMRC in the UK, including changes in tax rates, deductions, credits, and reporting requirements.

- Compliance involves correctly applying tax codes to business operations, ensuring eligibility for any available incentives, and avoiding prohibited practices such as tax evasion or misuse of loopholes.

- Engaging in ongoing education, consulting tax experts, and using reliable tax research tools help maintain alignment with current and emerging tax regulations.

What is the average salary for tax compliance officers in the accounting and tax compliance field?

Factors Influencing Tax Compliance Officer Salaries

- Geographic location plays a significant role in determining salary levels, with tax compliance officers in major metropolitan areas like New York, San Francisco, or Washington, D.C., typically earning higher wages due to the higher cost of living and greater demand for compliance expertise.

- Level of education and professional certifications strongly impact earnings; individuals with degrees in accounting, finance, or taxation, and those who hold credentials such as Certified Public Accountant (CPA) or Enrolled Agent (EA), are often compensated at higher rates.

- Years of experience directly correlate with salary growth, as entry-level compliance officers may start at modest wages, but professionals with 5 to 10 years of experience can see substantial increases, especially when they take on supervisory or specialized roles within compliance departments.

Average Salary Ranges in the United States

- According to data from the U.S. Bureau of Labor Statistics and various salary aggregation sites like Glassdoor and PayScale, the average annual salary for tax compliance officers in the United States typically ranges from $55,000 to $85,000 as of 2023–2024.

- Mid-career professionals with advanced skills in tax law interpretation, audit preparation, and regulatory reporting often earn between $70,000 and $95,000, particularly when employed by large accounting firms, corporations, or government agencies like the IRS.

- Senior compliance officers or those in managerial roles within federal or state tax authorities can earn upwards of $100,000 per year, with additional benefits such as performance bonuses, retirement contributions, and health packages further enhancing total compensation.

Industry and Employer Impact on Compensation

- Officers working in the public sector, including federal, state, or local government tax departments, often have standardized pay scales; for example, IRS revenue agents fall under the General Schedule pay scale, with salaries varying by GS grade and step, commonly ranging from $50,000 to $110,000 depending on location and seniority.

- Private sector employment, particularly in large accounting firms such as Deloitte, PwC, or EY, tends to offer competitive salaries and performance-based incentives, with tax compliance specialists earning between $60,000 and $90,000 on average, depending on client load and industry specialization.

- Corporations with in-house tax departments, especially in industries like finance, energy, or technology, may offer higher salaries to compliance officers due to the complexity of regulatory requirements, international tax obligations, and the need for real-time compliance monitoring, leading to total compensation packages that include bonuses and stock options.

Frequently Asked Questions

What is the difference between accounting and tax compliance?

Accounting involves recording, summarizing, and analyzing a company’s financial transactions to provide accurate financial information. Tax compliance, on the other hand, refers to adhering to tax laws and regulations by accurately calculating, reporting, and paying taxes on time. While accounting provides the data needed for tax filing, tax compliance ensures legal obligations are met with tax authorities, minimizing penalties and audit risks.

Why is tax compliance important for small businesses?

Tax compliance is crucial for small businesses to avoid fines, penalties, and legal issues. Proper compliance builds credibility with tax authorities and financial institutions. It ensures accurate reporting of income and expenses, supports long-term financial health, and helps in qualifying for loans or grants. Maintaining compliance also reduces the risk of audits and enhances the business’s reputation with customers, suppliers, and regulators.

How often should businesses review their accounting records for tax compliance?

Businesses should review their accounting records monthly to ensure accuracy and prepare for tax compliance. Regular reviews help detect errors early, track income and expenses, and maintain organized financial statements. Quarterly assessments are essential for estimated tax payments, while an annual review ensures all tax documentation is complete before filing. Consistent monitoring supports timely and accurate tax reporting.

What are common tax compliance requirements for businesses?

Common tax compliance requirements include timely filing of income tax returns, payroll tax reports, sales tax returns, and maintaining accurate financial records. Businesses must also comply with tax withholding regulations, issue 1099s or equivalent forms, and adhere to deadlines set by local, state, and federal tax authorities. Staying updated on tax law changes and maintaining proper documentation is essential to remain compliant and avoid penalties.

Leave a Reply