Advance tax compliance

Advance tax compliance refers to proactive measures taken by individuals and businesses to meet their tax obligations before deadlines, ensuring accuracy and adherence to evolving regulations.

As tax authorities worldwide enhance scrutiny and enforcement, staying ahead of compliance requirements minimizes risks of penalties, audits, and reputational damage. This approach involves timely reporting, correct withholding, proper documentation, and leveraging technology for efficient tax management.

In an era of digital transformation and international tax transparency initiatives, advance compliance supports financial stability and fosters trust with regulatory bodies. Understanding its importance is essential for navigating complex tax systems and achieving long-term fiscal responsibility in a globally interconnected economy.

Understanding Advance Tax Compliance: A Strategic Approach to Meeting Tax Obligations

Advance tax compliance refers to the proactive management and fulfillment of tax responsibilities before the official due dates set by tax authorities. This approach enables individuals and businesses to avoid penalties, reduce audit risks, and maintain financial stability by ensuring timely and accurate tax payments.

Particularly relevant in jurisdictions where income is not subject to withholding—such as for self-employed professionals or investors—advance tax compliance typically involves making periodic estimated tax payments throughout the fiscal year.

These payments are based on projected income and applicable tax rates, helping taxpayers align their liabilities with their earnings in real time. By embracing advance tax compliance, entities demonstrate fiscal responsibility, enhance transparency with tax authorities, and mitigate the burden of large, lump-sum tax payments at year-end.

Key Benefits of Advance Tax Compliance

One of the most significant advantages of advance tax compliance is the reduction of financial stress associated with unexpected tax liabilities. By estimating tax obligations in advance and making regular payments, taxpayers can better manage cash flow and avoid last-minute scrambles to gather funds before deadlines.

This method also minimizes the risk of penalties and interest charges that arise from underpayment or late payment of taxes. For businesses, consistent compliance strengthens credibility with regulatory bodies and can positively impact borrowing capacity and investor confidence.

Moreover, the process encourages accurate recordkeeping and a deeper understanding of one’s tax profile, allowing for more informed financial planning and strategic decision-making throughout the year.

Who Is Required to Make Advance Tax Payments?

Advance tax payments are generally required for individuals and entities whose income is not subject to sufficient withholding, such as freelancers, independent contractors, business owners, and investors receiving dividends or capital gains.

In the United States, for example, the IRS mandates estimated tax payments if you expect to owe at least $1,000 in tax after subtracting withholdings and credits. Similarly, corporations typically must pay estimated taxes if they expect to owe $500 or more when filing their return.

Requirements may vary by country, but common criteria include earning income from sources like self-employment, interest, rent, alimony, or capital gains. Failure to comply can lead to underpayment penalties, underscoring the importance of assessing your tax profile regularly and engaging in proactive planning.

How to Calculate and Schedule Advance Tax Payments

Calculating advance tax payments involves estimating your annual taxable income, determining the corresponding tax liability, and dividing payments into installments aligned with government deadlines.

In the U.S., these payments are typically due quarterly—April 15, June 15, September 15, and January 15 of the following year. To ensure accuracy, taxpayers can use the IRS Form 1040-ES worksheet or leverage tax software that factors in income, deductions, and credits.

Two common methods are used: the regular installments method, which applies a uniform percentage to each period, and the annualized income installment method, which adjusts for fluctuating earnings—ideal for seasonal businesses. Timely and accurate filing preserves compliance status and supports long-term financial health.

| Aspect | Detail | Relevance |

|---|---|---|

| Payment Frequency | Quarterly in most countries | Ensures consistent compliance and prevents year-end surges |

| Threshold for Individuals (U.S.) | Expected tax owed of at least $1,000 | Determines if estimated payments are mandatory |

| Penalty Avoidance | Pay at least 90% of current year tax or 100–110% of prior year | Helps taxpayers meet safe harbor rules |

| Key Calculation Tool | IRS Form 1040-ES or tax software | Supports accurate estimation of liability |

| Special Cases | Farmers, fishermen, and high-income earners have different rules | Highlights need for personalized tax planning |

Advanced Tax Compliance: A Comprehensive Guide to Staying Compliant

What are the key compliance requirements for advance tax payments?

Frequency and Timing of Advance Tax Payments

The frequency and timing of advance tax payments vary depending on the country's tax regulations, but generally follow a quarterly or monthly schedule.

Taxpayers are required to predict their annual tax liability and make payments at specified intervals to avoid penalties. Missing the deadline for any installment can result in interest charges or financial penalties. It’s essential for individuals and businesses to observe due dates set by the tax authority to maintain compliance.

- In most jurisdictions, advance tax payments are due in four equal installments throughout the fiscal or calendar year, typically aligned with quarter ends.

- Some countries require monthly payments for businesses or individuals with higher projected tax liabilities to ensure even revenue flow to the government.

- Payment deadlines are strictly enforced, and it's the taxpayer’s responsibility to anticipate due dates, even if no reminder is issued by the tax agency.

Accurate Estimation of Tax Liability

One of the fundamental compliance requirements is the accurate estimation of the annual tax liability. Taxpayers must base their advance payments on a reasonable projection of income, deductions, and applicable tax rates.

Underestimating tax obligations can lead to interest accrual or underpayment penalties, while overestimation may result in delayed refunds without interest. Proper record-keeping and periodic review of financial performance help ensure accurate estimations.

- Taxpayers must analyze prior year returns, current income trends, and anticipated changes in deductions or credits to forecast their tax burden realistically.

- In certain regions, safe harbor rules allow taxpayers to avoid underpayment penalties by paying either 90% of the current year’s liability or 100%–110% of the prior year’s tax, depending on income level.

- Businesses often use accounting software or consult tax professionals to update and refine their estimates each payment period for greater accuracy.

Documentation and Reporting Obligations

Alongside timely payments, taxpayers must adhere to formal reporting requirements to substantiate their advance tax deposits. This includes maintaining detailed records of payments, submitting required forms, and reconciling estimates with actual tax owed at year-end. The tax authority may audit these records to verify compliance, making organized documentation a critical component of the process.

- Taxpayers must keep proof of each advance payment, such as bank transaction records or receipts issued by tax authorities, to support their filings in case of an audit.

- Some countries require submission of periodic reports or declarations detailing the amount of tax paid and the basis of the estimation used.

- At the end of the year, a reconciliation process compares total advance payments to the final tax liability, and any difference must be either refunded or settled through an additional payment.

What does advance tax compliance entail?

Definition and Purpose of Advance Tax Compliance

- Advance tax compliance refers to the process by which taxpayers estimate, report, and pay their expected tax liability before the actual tax assessment or filing deadline. This practice ensures that tax authorities receive revenue in a timely and predictable manner, reducing the risk of large, unexpected shortfalls at the end of a fiscal period.

- It is commonly required for individuals and businesses that earn income not subject to withholding taxes, such as self-employment income, rental income, or investment returns. By making advance payments, taxpayers avoid penalties for underpayment and demonstrate proactive adherence to tax regulations.

- Advance tax compliance systems are designed to align taxpayer payments with their earning patterns throughout the year, especially in jurisdictions where annual lump-sum tax settlement may pose cash flow challenges for both governments and individuals.

Key Components of Advance Tax Payments

- One primary component is the estimation of annual taxable income, which taxpayers must calculate based on previous earnings, contracts, or projected profits. Accuracy in this calculation helps minimize adjustments during final tax assessment and reduces the likelihood of interest charges.

- Another component involves adhering to scheduled payment deadlines, often set quarterly or monthly depending on the country’s fiscal calendar. Municipal, state, and federal tax agencies typically publish specific due dates that taxpayers must follow meticulously.

- The third component includes the submission of documentation or forms that substantiate the advance payments made. These may include payment vouchers, self-declared income schedules, or digital filings integrated with national tax portals to ensure traceability and record-keeping.

Implications of Non-Compliance with Advance Tax Rules

- Failing to make advance tax payments on time generally results in financial penalties, such as interest on overdue amounts calculated from the due date to the date of payment. These charges accumulate over time, increasing the total tax burden for the individual or business.

- Repeated non-compliance may trigger audits or increased scrutiny from tax authorities, potentially leading to comprehensive reviews of past returns and additional documentation requirements in future filings.

- In some jurisdictions, persistent failure to comply with advance tax obligations can lead to legal consequences, including asset freezes, wage garnishment, or restrictions on obtaining government services and licenses, thereby disrupting personal and business operations.

What are the consequences of failing to comply with advance tax payment requirements?

Penalties and Interest Charges

- Taxpayers who fail to meet advance tax payment requirements are typically subject to financial penalties imposed by tax authorities. These penalties are designed to encourage timely compliance and vary depending on the jurisdiction and extent of the shortfall.

- In addition to penalties, unpaid advance tax amounts usually accrue interest from the original due date until the date of full payment. This interest is computed at a statutory rate, which may be adjusted quarterly or annually, further increasing the taxpayer’s liability over time.

- The combination of penalties and interest can significantly inflate the total amount owed, particularly if the non-compliance persists across multiple tax periods, making it more burdensome for individuals and businesses to settle their tax obligations.

Increased Scrutiny and Audit Risk

- Failing to make required advance tax payments may trigger increased attention from tax authorities, leading to a higher probability of being selected for audit or review. Tax agencies often use compliance history as a factor in determining audit selection.

- Audits resulting from non-compliance can be time-consuming and resource-intensive, requiring the taxpayer to provide extensive documentation to justify income, expenses, and tax calculations.

- Repeated failure to meet advance payment obligations could establish a pattern of non-compliance, making the taxpayer more likely to be audited in future years, even if subsequent payments are made on time.

Cash Flow and Financial Planning Challenges

- When advance tax payments are missed, the accumulated tax liability is often due in a lump sum at the end of the tax year, which can create severe cash flow problems, especially for small businesses or self-employed individuals.

- Inadequate tax planning and reliance on deferring payments may disrupt budgeting efforts, limit access to capital for business investments, and strain personal or corporate financial management.

- The financial stress from unexpected large tax bills can result in the need to take on debt, sell assets, or delay other essential expenses, ultimately affecting long-term financial stability.

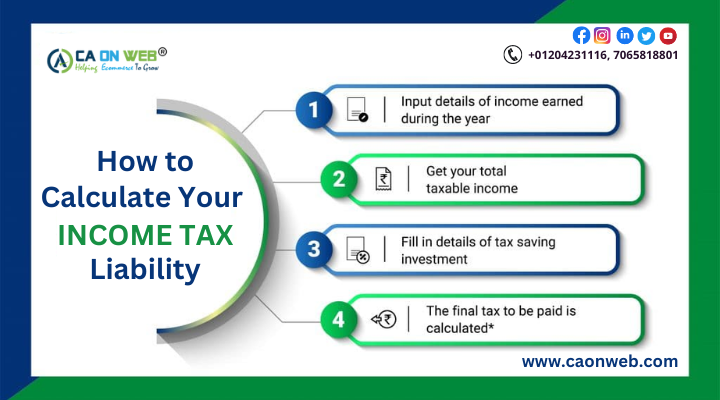

What is the process for calculating my advance tax liability for compliance?

To calculate your advance tax liability for compliance, you must estimate your total annual tax obligation based on projected income and applicable tax rates, then pay it in periodic installments as required by your local tax authority.

This process ensures that taxpayers with substantial non-salary income—such as from freelancing, business operations, investments, or rental sources—contribute taxes throughout the year rather than in a lump sum at year-end.

The exact method and deadlines for these payments vary by jurisdiction, but generally involve analyzing previous year earnings, forecasting current-year income, applying relevant tax slabs or rates, deducting allowable expenses and credits, and dividing the resulting tax amount into installments, often quarterly or monthly. Failure to pay advance tax on time can result in interest penalties, so accurate forecasting and timely payments are essential for compliance.

1. Determine If You Are Required to Pay Advance Tax

- First, assess whether your tax jurisdiction mandates advance tax payments; typically, these requirements apply if your annual tax liability exceeds a specified threshold after subtracting tax deducted at source (TDS).

- For instance, in countries like India, if your tax liability is INR 10,000 or more in a financial year, you are generally required to pay advance tax; self-employed individuals, professionals, and investors often fall into this category.

- Employees whose income is primarily from salary might not need to pay advance tax separately if their employer withholds sufficient tax via TDS, but additional income sources may trigger the obligation.

2. Estimate Your Annual Income and Taxable Amount

- Gather all sources of income expected during the financial year, such as business income, professional fees, interest, capital gains, rental income, and other taxable receipts.

- Deduct allowable business expenses, depreciation, applicable tax exemptions, and deductions under relevant sections (e.g., Section 80C in India) to arrive at your net taxable income.

- Apply the current year’s income tax rates or slab system to calculate your estimated total tax liability, including any surcharges or health and education cess that may apply.

3. Schedule and Make Installment Payments

- Divide the estimated tax liability into installments according to the due dates specified by tax authorities; for example, in India, advance tax is paid in four installments due by June 15, September 15, December 15, and March 15.

- Each installment typically requires a cumulative assessment: the first payment should cover at least 15% of total liability, the second at least 45%, and the third at least 75%, with the final payment settling any remaining amount.

- Payments must be made through official channels such as online tax payment portals, and you must retain the challan or acknowledgment as proof; adjustments can be made in later installments if income projections change significantly during the year.

Frequently Asked Questions

What is advance tax compliance?

Advance tax compliance refers to fulfilling tax obligations before the due date, often through estimated tax payments made during the year. It ensures individuals and businesses meet their tax liabilities on time, avoiding penalties.

This process applies to income not subject to withholding, such as self-employment earnings. Many countries require quarterly payments based on projected annual income, promoting consistent revenue collection and financial accountability.

Who needs to follow advance tax compliance?

Individuals, freelancers, and businesses with income not subject to tax withholding must follow advance tax compliance. This typically includes self-employed professionals, investors, and those with rental or foreign income.

Employees whose tax is fully withheld by employers are usually exempt. Requirements vary by country, but generally, if you expect to owe a certain minimum tax amount, you must make periodic advance payments to remain compliant.

How are advance tax payments calculated?

Advance tax payments are calculated using estimated annual income and applicable tax rates. Taxpayers assess their expected earnings, deduct allowable expenses, and apply the relevant tax bracket.

Payments are often split into installments—quarterly or monthly—depending on local regulations. Accurate estimation helps avoid underpayment penalties. Using prior year tax data can assist in making reliable projections for current year liabilities.

What are the consequences of missing advance tax deadlines?

Missing advance tax deadlines typically results in interest charges and penalties. Tax authorities impose these to encourage timely compliance and compensate for delayed revenue.

The severity depends on the amount owed and how late the payment is. In some cases, continuous non-compliance may trigger audits or legal action. Promptly rectifying missed payments can reduce additional fees and maintain good standing with tax agencies.

Leave a Reply